ENVIRONMENTAL, SOCIAL AND

GOVERNANCE (ESG) SURVEY

CFA Institute

June 2015

�. TABLE OF CONTENTS

About The Survey

03

Survey Results

04

Respondent Profile

17

Appendix: Data Tables & Comments

20

2

�. ABOUT THE SURVEY

Background & Purpose

The purpose of this survey is to better understand the perceptions of CFA

Institute membership concerning ESG issues and ESG data, as well as how

members use such information in their investing processes.

Methodology

On 26 May 2015, 44,131 CFA Institute members that are portfolio managers and

research analysts were invited via email to participate in an online survey. The

survey closed on 5 June 2015. 1,325 valid responses were received, for a

response rate of 3% and a margin of error of ± 2.7%.

3

�. SURVEY RESULTS

4

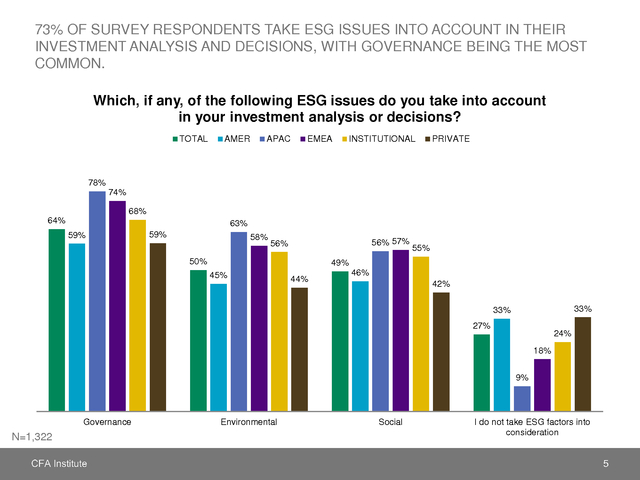

�. 73% OF SURVEY RESPONDENTS TAKE ESG ISSUES INTO ACCOUNT IN THEIR

INVESTMENT ANALYSIS AND DECISIONS, WITH GOVERNANCE BEING THE MOST

COMMON.

Which, if any, of the following ESG issues do you take into account

in your investment analysis or decisions?

TOTAL

AMER

APAC

EMEA

INSTITUTIONAL

PRIVATE

78%

74%

68%

64%

63%

59%

59%

58%

56% 57%

56%

50%

55%

49%

45%

44%

46%

42%

33%

33%

27%

24%

18%

9%

Governance

N=1,322

Environmental

Social

I do not take ESG factors into

consideration

5

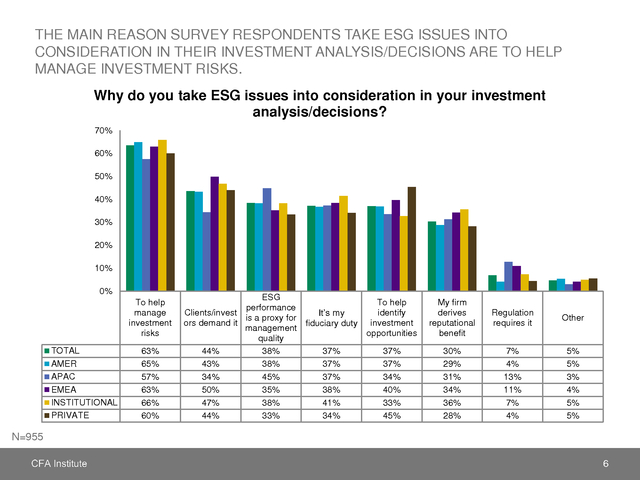

�. THE MAIN REASON SURVEY RESPONDENTS TAKE ESG ISSUES INTO

CONSIDERATION IN THEIR INVESTMENT ANALYSIS/DECISIONS ARE TO HELP

MANAGE INVESTMENT RISKS.

Why do you take ESG issues into consideration in your investment

analysis/decisions?

70%

60%

50%

40%

30%

20%

10%

0%

To help

manage

investment

risks

TOTAL

AMER

APAC

EMEA

INSTITUTIONAL

PRIVATE

63%

65%

57%

63%

66%

60%

ESG

To help

performance

Clients/invest

identify

It’s my

is a proxy for

ors demand it

fiduciary duty investment

management

opportunities

quality

44%

38%

37%

37%

43%

38%

37%

37%

34%

45%

37%

34%

50%

35%

38%

40%

47%

38%

41%

33%

44%

33%

34%

45%

My firm

derives

reputational

benefit

Regulation

requires it

Other

30%

29%

31%

34%

36%

28%

7%

4%

13%

11%

7%

4%

5%

5%

3%

4%

5%

5%

N=955

6

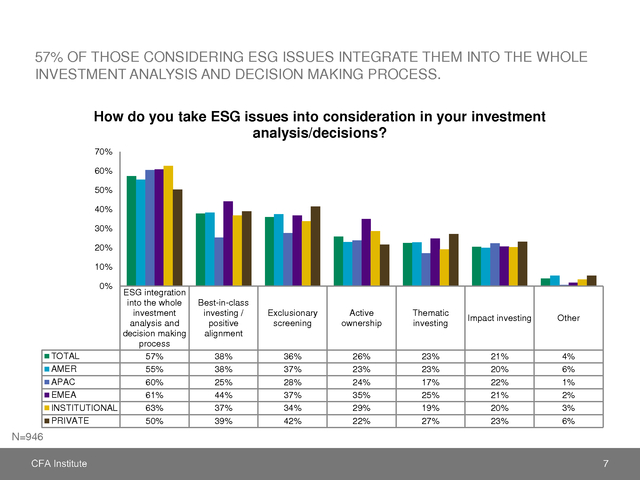

�. 57% OF THOSE CONSIDERING ESG ISSUES INTEGRATE THEM INTO THE WHOLE

INVESTMENT ANALYSIS AND DECISION MAKING PROCESS.

How do you take ESG issues into consideration in your investment

analysis/decisions?

70%

60%

50%

40%

30%

20%

10%

0%

ESG integration

into the whole

investment

analysis and

decision making

process

TOTAL

57%

AMER

55%

APAC

60%

EMEA

61%

INSTITUTIONAL

63%

PRIVATE

50%

Best-in-class

investing /

positive

alignment

Exclusionary

screening

Active

ownership

Thematic

investing

Impact investing

Other

38%

38%

25%

44%

37%

39%

36%

37%

28%

37%

34%

42%

26%

23%

24%

35%

29%

22%

23%

23%

17%

25%

19%

27%

21%

20%

22%

21%

20%

23%

4%

6%

1%

2%

3%

6%

N=946

7

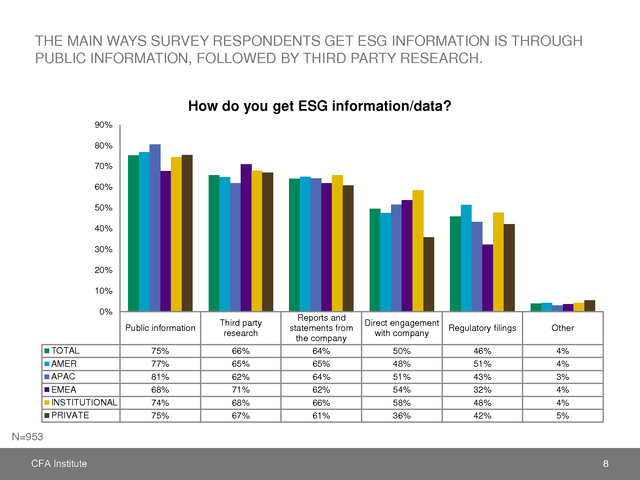

�. THE MAIN WAYS SURVEY RESPONDENTS GET ESG INFORMATION IS THROUGH

PUBLIC INFORMATION, FOLLOWED BY THIRD PARTY RESEARCH.

How do you get ESG information/data?

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Public information

TOTAL

AMER

APAC

EMEA

INSTITUTIONAL

PRIVATE

Third party

research

75%

77%

81%

68%

74%

75%

66%

65%

62%

71%

68%

67%

Reports and

statements from

the company

64%

65%

64%

62%

66%

61%

Direct engagement

with company

Regulatory filings

Other

50%

48%

51%

54%

58%

36%

46%

51%

43%

32%

48%

42%

4%

4%

3%

4%

4%

5%

N=953

8

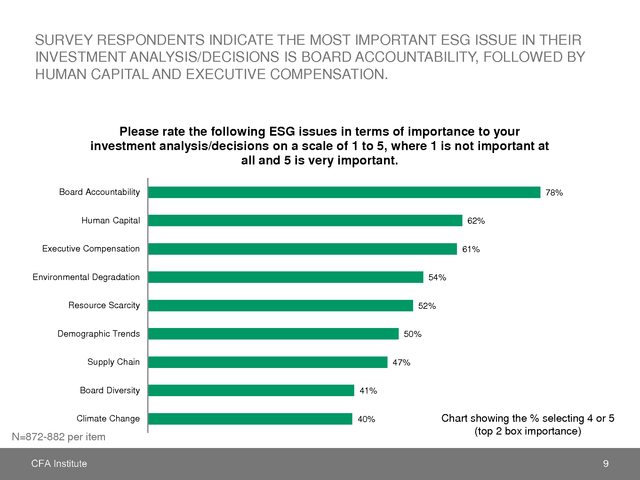

�. SURVEY RESPONDENTS INDICATE THE MOST IMPORTANT ESG ISSUE IN THEIR

INVESTMENT ANALYSIS/DECISIONS IS BOARD ACCOUNTABILITY, FOLLOWED BY

HUMAN CAPITAL AND EXECUTIVE COMPENSATION.

Please rate the following ESG issues in terms of importance to your

investment analysis/decisions on a scale of 1 to 5, where 1 is not important at

all and 5 is very important.

Board Accountability

78%

Human Capital

62%

Executive Compensation

61%

Environmental Degradation

54%

Resource Scarcity

52%

Demographic Trends

50%

Supply Chain

47%

Board Diversity

41%

Climate Change

40%

N=872-882 per item

Chart showing the % selecting 4 or 5

(top 2 box importance)

9

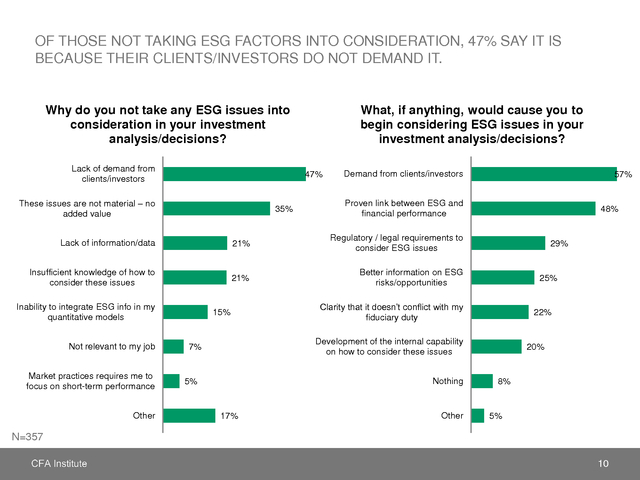

�. OF THOSE NOT TAKING ESG FACTORS INTO CONSIDERATION, 47% SAY IT IS

BECAUSE THEIR CLIENTS/INVESTORS DO NOT DEMAND IT.

Why do you not take any ESG issues into

consideration in your investment

analysis/decisions?

Lack of demand from

clients/investors

What, if anything, would cause you to

begin considering ESG issues in your

investment analysis/decisions?

47%

These issues are not material – no

added value

35%

Demand from clients/investors

57%

Proven link between ESG and

financial performance

Lack of information/data

21%

Regulatory / legal requirements to

consider ESG issues

Insufficient knowledge of how to

consider these issues

21%

48%

Better information on ESG

risks/opportunities

Inability to integrate ESG info in my

quantitative models

Not relevant to my job

Market practices requires me to

focus on short-term performance

Other

15%

29%

25%

Clarity that it doesn’t conflict with my

fiduciary duty

22%

Development of the internal capability

on how to consider these issues

7%

Nothing

5%

17%

Other

20%

8%

5%

N=357

10

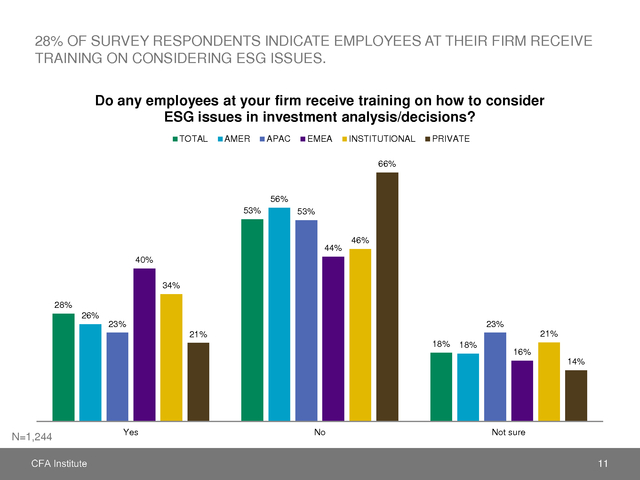

�. 28% OF SURVEY RESPONDENTS INDICATE EMPLOYEES AT THEIR FIRM RECEIVE

TRAINING ON CONSIDERING ESG ISSUES.

Do any employees at your firm receive training on how to consider

ESG issues in investment analysis/decisions?

TOTAL

AMER

APAC

EMEA

INSTITUTIONAL

PRIVATE

66%

56%

53%

53%

44%

46%

40%

34%

28%

26%

23%

23%

21%

21%

18%

18%

16%

14%

N=1,244

Yes

No

Not sure

11

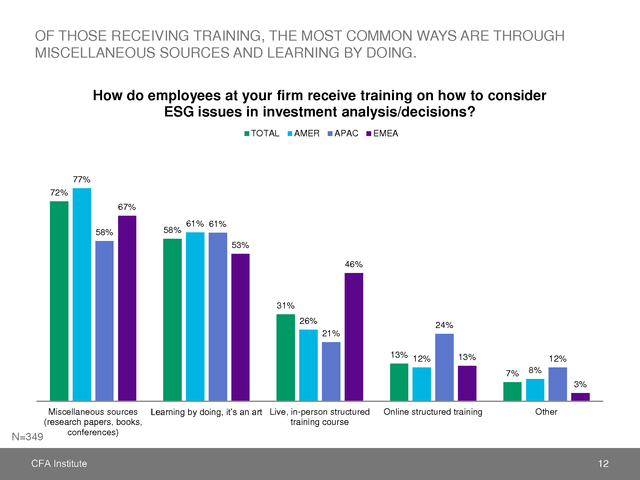

�. OF THOSE RECEIVING TRAINING, THE MOST COMMON WAYS ARE THROUGH

MISCELLANEOUS SOURCES AND LEARNING BY DOING.

How do employees at your firm receive training on how to consider

ESG issues in investment analysis/decisions?

TOTAL

AMER

APAC

EMEA

77%

72%

67%

58%

58%

61% 61%

53%

46%

31%

26%

24%

21%

13% 12%

13%

12%

7%

8%

3%

N=349

Miscellaneous sources Learning by doing, it’s an art Live, in-person structured

(research papers, books,

training course

conferences)

Online structured training

Other

12

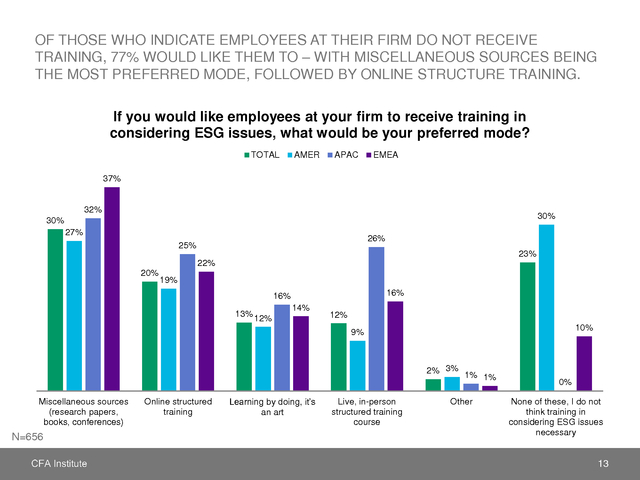

�. OF THOSE WHO INDICATE EMPLOYEES AT THEIR FIRM DO NOT RECEIVE

TRAINING, 77% WOULD LIKE THEM TO – WITH MISCELLANEOUS SOURCES BEING

THE MOST PREFERRED MODE, FOLLOWED BY ONLINE STRUCTURE TRAINING.

If you would like employees at your firm to receive training in

considering ESG issues, what would be your preferred mode?

TOTAL

AMER

APAC

EMEA

37%

32%

30%

30%

27%

26%

25%

23%

22%

20%

19%

16%

16%

13% 12%

14%

12%

10%

9%

2% 3%

Miscellaneous sources

(research papers,

books, conferences)

N=656

Online structured

training

Learning by doing, it’s

an art

Live, in-person

structured training

course

1% 1%

Other

0%

None of these, I do not

think training in

considering ESG issues

necessary

13

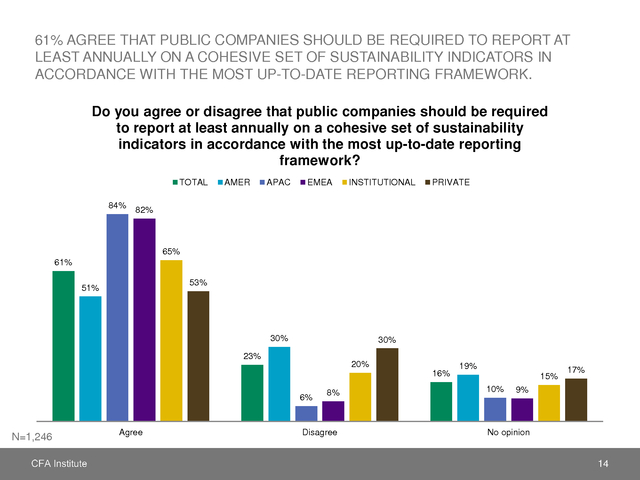

�. 61% AGREE THAT PUBLIC COMPANIES SHOULD BE REQUIRED TO REPORT AT

LEAST ANNUALLY ON A COHESIVE SET OF SUSTAINABILITY INDICATORS IN

ACCORDANCE WITH THE MOST UP-TO-DATE REPORTING FRAMEWORK.

Do you agree or disagree that public companies should be required

to report at least annually on a cohesive set of sustainability

indicators in accordance with the most up-to-date reporting

framework?

TOTAL

84%

AMER

APAC

EMEA

INSTITUTIONAL

PRIVATE

82%

65%

61%

53%

51%

30%

30%

23%

20%

16%

6%

N=1,246

Agree

8%

Disagree

19%

15%

10%

17%

9%

No opinion

14

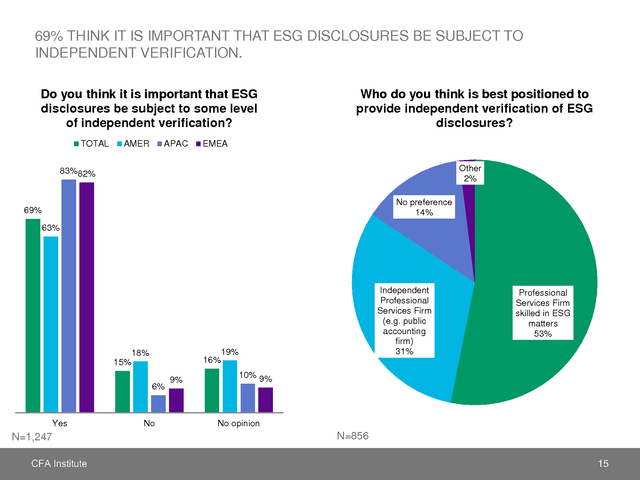

�. 69% THINK IT IS IMPORTANT THAT ESG DISCLOSURES BE SUBJECT TO

INDEPENDENT VERIFICATION.

Do you think it is important that ESG

disclosures be subject to some level

of independent verification?

TOTAL

AMER

APAC

Who do you think is best positioned to

provide independent verification of ESG

disclosures?

EMEA

Other

2%

83%82%

No preference

14%

69%

63%

18%

16%

15%

6%

Yes

N=1,247

No

9%

Independent

Professional

Services Firm

(e.g. public

accounting

firm)

31%

19%

Professional

Services Firm

skilled in ESG

matters

53%

10% 9%

No opinion

N=856

15

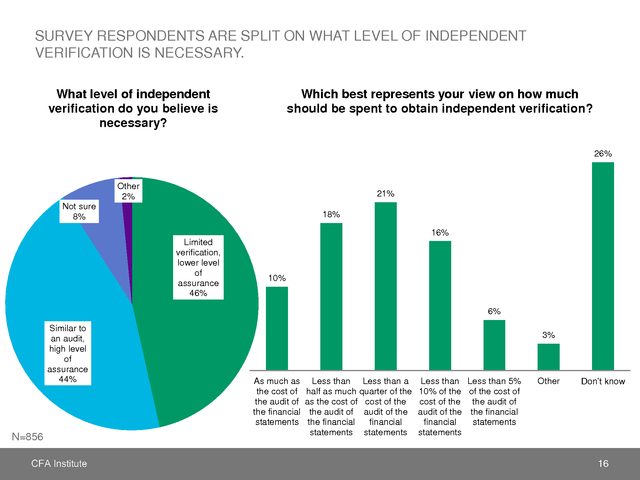

�. SURVEY RESPONDENTS ARE SPLIT ON WHAT LEVEL OF INDEPENDENT

VERIFICATION IS NECESSARY.

What level of independent

verification do you believe is

necessary?

Which best represents your view on how much

should be spent to obtain independent verification?

26%

Other

2%

21%

Not sure

8%

18%

16%

Limited

verification,

lower level

of

assurance

46%

10%

6%

Similar to

an audit,

high level

of

assurance

44%

N=856

3%

As much as

the cost of

the audit of

the financial

statements

Less than Less than a

half as much quarter of the

as the cost of cost of the

the audit of audit of the

the financial

financial

statements statements

Less than Less than 5%

10% of the of the cost of

cost of the the audit of

audit of the the financial

financial

statements

statements

Other

Don’t know

16

�. RESPONDENT PROFILE

17

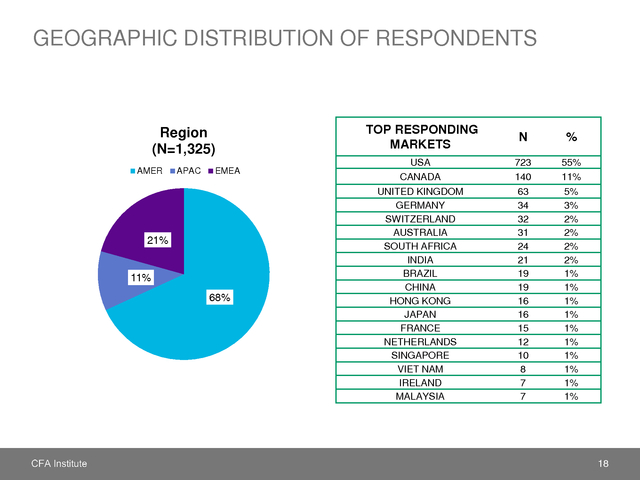

�. GEOGRAPHIC DISTRIBUTION OF RESPONDENTS

Region

(N=1,325)

AMER

APAC

EMEA

21%

11%

68%

TOP RESPONDING

MARKETS

N

%

USA

CANADA

723

140

55%

11%

UNITED KINGDOM

GERMANY

SWITZERLAND

AUSTRALIA

SOUTH AFRICA

INDIA

BRAZIL

CHINA

HONG KONG

JAPAN

FRANCE

NETHERLANDS

SINGAPORE

VIET NAM

IRELAND

MALAYSIA

63

34

32

31

24

21

19

19

16

16

15

12

10

8

7

7

5%

3%

2%

2%

2%

2%

1%

1%

1%

1%

1%

1%

1%

1%

1%

1%

18

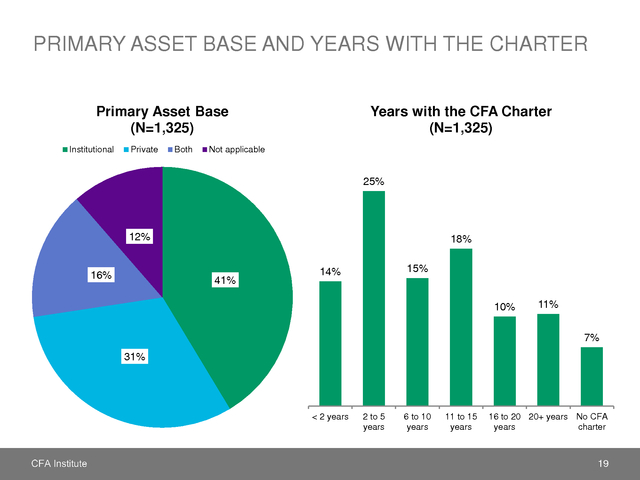

�. PRIMARY ASSET BASE AND YEARS WITH THE CHARTER

Primary Asset Base

(N=1,325)

Institutional

Private

Both

Years with the CFA Charter

(N=1,325)

Not applicable

25%

12%

16%

18%

41%

15%

14%

10%

11%

7%

31%

< 2 years

2 to 5

years

6 to 10

years

11 to 15

years

16 to 20 20+ years No CFA

years

charter

19

�.