Outlook for Nordic PE:

An insider perspective

on 2016

Despite rising valuations, PE professionals

are optimistic about the year 2016

�. II

White & Case

�. Outlook for Nordic PE:

An insider perspective on 2016

Private equity professionals identify strategies that firms are pursuing to drive

growth even as competition remains fierce

By Ulf Johansson, Lennart Pettersson and Henrik Wireklint

I

n 2016, private equity (PE) in the

Nordic region is likely to meet

or exceed 2015 performance,

according to investment

professionals we interviewed early

this year. But insiders also say that

firms are adjusting their business

models to account for new realities,

such as the persistence of high

valuations that have significantly

raised the hurdle for profitability of

portfolio companies

In the first two months of this year,

we conducted extensive interviews

with 15 investment professionals

from leading Stockholm PE firms to

get their perspectives on the Nordic

market. All were optimistic about

2016, but the professionals also

highlighted a number of challenging

trends stemming from increasing

competition for good deals.

Chief among these was

the need for firms to focus on

operational excellence and build

industry expertise to ensure they

maximize the value of their portfolio

companies. Virtually every firm sees

this as critical at a time when high

valuations continue to threaten

return on investment (ROI).

Many are also adopting new

criteria for identifying targets with

greater ROI potential.

That may

involve specializing in more complex

deals that other buyers lack the

skills to handle, or focusing more on

market or regional niches that are

not on competitors’ radar.

Most investment professionals

said that firms will continue with

co-investments, which enable

them to pursue deals that they

might not otherwise be able to

finance. And firms are increasingly

likely to purchase M&A insurance

to hedge their risks in this highstakes environment.

But despite some challenges,

investment professionals didn’t

waver in their belief that Nordic

PE will see a continuation of the

positive performance that has been

characteristic of the region in

recent years.

and then making a well-timed exit is

no longer enough, these experts say.

Firms are increasingly recruiting

industry experts to ensure that the

management teams of portfolio

companies get enhanced support

from PE funds to fuel industrial value

creation. For example, Stockholmbased EQT AB has recruited Henrik

Landgren, former VP of Analytics at

Spotify, and Andreas Thorstensson,

co-founder of Toborrow, both of

whom will add tech expertise to

EQT’s venture fund table.

Jerseybased Nordic Capital has recruited

Olof Faxander, former CEO of

Sandvik and SSAB, two of Sweden’s

flagship industrial companies, as

operating partner and co-head of its

Operations team.

A new watchword:

“operational excellence”

Asked about their top business

priorities for 2016, nearly all

interviewees cited the need

to build up their capacity for

bringing “operational excellence”

to portfolio companies.

The traditional PE progression of

identifying attractive assets, buying

them at a favourable multiple,

ensuring a robust management team

Having industry experts on the

team reassures portfolio companies

that the fund is serious about

creating real industry value.

Outlook for Nordic PE: An Insider Perspective on 2016

�. Interviewees say having such

figures on the team reassures

portfolio companies that the PE

fund is serious about creating real

industry value—which is all the more

critical when assets are purchased

at high multiples. Diversifying the

background and bolstering the

expertise of the PE funds’ own

advisory teams in this way helps

deflect the persistent criticism that

PE funds lack sufficient industry

expertise to be successful active

owners. Demonstrating these

internal competencies to potential

fund investors may aid fundraising,

as well.

And this approach can help

persuade industrial sellers who may

be reluctant to sell to PE funds,

according to interviewees. Family

and partner-owned businesses in

particular are easier to win over when

sellers have confidence that the

target company will continue to be

run by someone who understands

them and their business.

High multiples spark

a search for ROI

All of the investment professionals

we interviewed said they expected

their firms to do at least as many

deals in 2016 as in 2015, and several

expected to do more.

But continued

high multiples are affecting how

these firms choose their targets.

One executive said his firm plans

to seek out more complex and

challenging transactions in the hope

of avoiding competition and securing

more attractive multiples. Others

plan to target regional markets or

business sectors where current

valuations remain more attractive

than in other regions or sectors.

For example, US healthcare

companies may offer lower, more

attractive multiples than do Nordic

and other European healthcare

companies, and Swedish software

companies may make more

attractive targets when located

outside of the Stockholm area

where multiples may be inflated,

interviewees say.

2

White & Case

Because 2015 was such a

robust year for Nordic IPOs, the

mid-size and large-cap M&A

sector has shrunk, and investors

are watching to see if the volatility

in Nordic stock exchanges at the

start of the year will lead to an

increase in M&A exits in 2016.

Most interviewees expect the

IPO window to remain open in

2016, but they also expect the

number of IPOs to go down.

Some noted that the especially

high volatility in exchanges at the

time of the interview had made

them think twice before initiating

a new IPO, and that trade sales

may be preferable for many

2016 exits. A few interviewees

predicted that the IPO window

may close for a long time due

to erratic market behavior.

Every fund is looking for a sweet

spot away from the high multiples

of secondary exits.

Market volatility may give rise

to more specialist funds and a

sharper industry focus in the small

PE fund segment, where every

fund is looking for a sweet spot

away from the high multiples

of secondary exits.

Although PE funds will still be

looking to participate in auction

processes initiated by their

competitors, the interviewees

say they are becoming somewhat

more skittish where auctions are

in play, as auctions can

drive up prices past the point

where achieving sufficient ROI

remains likely.

Co-investments are here

to stay

Nearly all interviewees said taking

on co-investors will continue to be

common practice, at least among

mid-size and large PE funds.

Most such funds have commitments

to certain investors to offer coinvestment opportunities and have

gradually streamlined the process

of onboarding co-investors into

new deals.

While co-investment can reduce

management fees for PE firms,

they can also increase the amount

of funding that PE firms are able

to raise.

This can enable them

to compete for deals that might

otherwise be out of reach. Some

interviewees said that they like

co-investments because they

can help the PE firm to assemble

valuable business competence

for closing the deal and for raising

value post-closing.

Co-investments that involve

a group of many small, passive

investors are often more attractive

than those that involve only one or

a few active minority investors, the

interviewees say.

Investors are attracted to coinvestment options because they

usually give investors more control.

In particular, co-investors typically

play a significant role in selecting the

targets that the PE firm invests in

over the life of the fund.

Co-investments do add to the

administrative burden for PE firms,

increasing the resources they

have to expend to accommodate

investor requests for information and

manage how they interact with the

fund. Co-investments also add to

the complexity of executing deals,

requiring internal deal teams and

external deal counsel to manage

co-investment details in parallel

with transaction workstreams.

But

investment professionals say the

increased burden is manageable,

and that the results often justify the

extra effort.

Interviewees say that they may

sometimes wait to enter into

co-investments until after signing

a deal, but that they do so only

after careful consideration of the

increased risk. Those that wait could

fail to find co-investors and may

have to shoulder the full investment

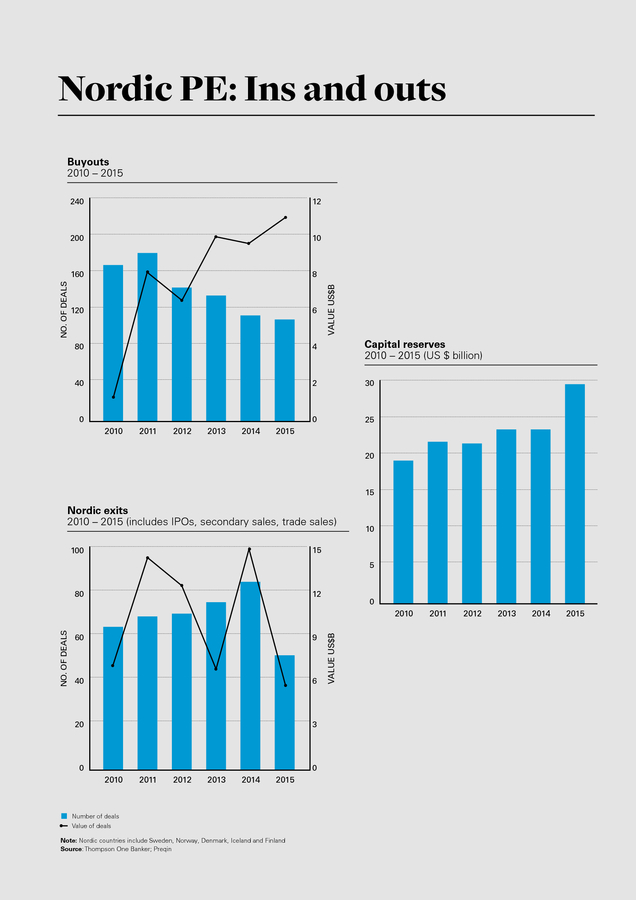

�. Nordic PE: Ins and outs

Buyouts

2010 – 2015

10

160

8

120

6

80

4

Capital reserves

2010 – 2015 (US $ billion)

40

2

30

0

25

0

2010

2011

2012

2013

2014

VALUE US$B

12

200

NO. OF DEALS

240

2015

20

15

Nordic exits

2010 – 2015 (includes IPOs, secondary sales, trade sales)

10

15

100

5

12

80

0

60

9

40

6

20

3

0

0

2010

2011

2012

2013

2014

2015

Number of deals

Value of deals

Note: Nordic countries include Sweden, Norway, Denmark, Iceland and Finland

Source: Thompson One Banker; Preqin

VALUE US$B

NO. OF DEALS

2010

2011

2012

2013

2014

2015

�. themselves. This could put them

in breach of investment terms

they have with existing investors

in their fund. Of course, the

risk is eliminated in cases when

the share purchase agreement

for a deal contains a condition

precedent, such as an equity

financing-out, that enables the

firm to walk away from the

deal if it can’t obtain sufficient

co-investment.

M&A insurance

gains popularity

Use of M&A insurance will continue

to rise, according to interviewees,

particularly for seller-initiated auction

processes. Nearly all interviewees

said that they consider M&A

insurance for every investment and

exit case they evaluate.

But when deal terms are

considered attractive, Nordic PE

firms may still see the cost of

M&A insurance as too high for an

exit relative to the risk and decline

to buy it.

The scope and premiums for

tax and environmental warranties

could also dissuade firms from

buying insurance.

Depending on

the operational footprint of the

target company, protections for

environmental and tax warranties

may be very expensive while still

not offering exhaustive coverage.

And where a fund is hoping

to pre-empt an auction process,

the aggressive pace at which

such transactions play out can

prevent a fund from acquiring

insurance, given the time insurers

may demand for checking the

buyer’s due diligence and the

time the buyer may need to

make corrections the insurer

wants. Such transactions may

proceed without insurance, unless

the seller has already obtained

insurance to cover the deal.

White & Case

Most interviewees agreed that

long-term clarity on the tax situation

in the Nordic region is a top priority.

Some blame the tax uncertainty

for the decision by several offshore

funds to postpone plans to bring

funds onshore, and representatives

of onshore funds said adverse tax

rulings could make them consider

moving to offshore structures.

Most interviewees were also

concerned about continued negative

coverage of PE firms in the media,

which they believe is responsible

for poor public perceptions of the

sector. Some PE firms have made

changes to how they do business

in reaction to media coverage.

* * *

Dynamics have changed for Nordic

PE in recent years, but leading

firms are adapting in ways that will

enable them to continue to grow.

Most agree that the sector’s positive

performance will continue at least

through 2016.

n

Acknowledgements

Johan Steen, Rikard Stenberg,

Oscar Liljeson and Christian

Holmberg also contributed

to this effort.

Onshore funds said adverse tax

rulings could make them consider

moving to offshore structures.

For example, although they

may continue to invest in welfarerelated targets, some PE funds

may be less likely to take on such

investments in the short term in

order to steer clear of any mediagenerated controversy that might

have the potential to damage the

deal’s success for all parties.

To combat PE’s PR problem,

many firms have made efforts

to increase transparency, and

some have ramped up their public

relations activity (in the past, firms

tended not to respond to media

criticism). More PE funds are

also launching corporate social

responsibility programs, in part

to improve their public image.

NY0516/TL/GT/208165_7

4

Wild cards: Politics and

the media

�. �. Ulf Johansson

Partner, Stockholm

T +46 8 50632 311

E ulf.johansson@whitecase.com

Lennart Pettersson

Partner, Stockholm

T +46 8 50632 345

E lennart.pettersson@whitecase.com

whitecase.com

© 2016 White & Case LLP

VI

White & Case

�.